Sinking Funds Explained: Categories, Amounts & How to Start

You know that sinking feeling when a $1,200 car insurance bill arrives, or December hits and you haven't saved for holiday gifts? Sinking funds fix that. They're the budgeting tool that turns predictable financial stress into a non-event — by saving a small amount each month so the money is ready when you need it.

1. What Are Sinking Funds?

A sinking fund is money you save gradually for a planned future expense. The name comes from an old accounting term where companies "sank" money into a fund over time to cover future obligations like bond repayments.

In personal finance, sinking funds cover expenses that are predictable but not monthly. You know your car will need maintenance. You know December requires gift spending. You know your annual insurance premiums are coming. Sinking funds spread these costs across all 12 months so no single month breaks your budget.

Without sinking funds, these expenses feel like emergencies. Your car needs new tires ($600), so you put it on a credit card. Holiday gifts cost $800, so you carry a balance into January. Each "surprise" adds debt — but none of them were actually surprises. They were predictable expenses you didn't plan for.

2. Sinking Funds vs Emergency Fund

These serve different purposes and should be kept separate:

| Sinking Fund | Emergency Fund | |

|---|---|---|

| Purpose | Planned, expected expenses | Unexpected emergencies |

| Examples | Car maintenance, gifts, vacation, annual bills | Job loss, medical emergency, major repair |

| Timing | You know roughly when you will need it | You have no idea when (or if) you will need it |

| Spent regularly? | Yes — used and replenished throughout the year | Ideally never — it sits there for true emergencies |

| Target amount | Varies by category ($50-$300/month) | 3-6 months of essential expenses |

| Priority | After emergency fund is started | First financial priority |

3. Common Sinking Fund Categories

Here are the most popular sinking fund categories with typical annual costs and monthly savings targets:

| Category | Annual estimate | Monthly savings | Priority |

|---|---|---|---|

| Car maintenance & repairs | $1,200-2,000 | $100-170 | High |

| Holiday gifts | $500-1,500 | $42-125 | High |

| Vacation / travel | $1,000-3,000 | $85-250 | Medium |

| Medical / dental | $500-1,500 | $42-125 | High |

| Home maintenance | $1,000-3,000 | $85-250 | High (homeowners) |

| Annual insurance premiums | $1,200-2,400 | $100-200 | High |

| Clothing & shoes | $600-1,200 | $50-100 | Medium |

| Pet expenses | $500-1,500 | $42-125 | High (pet owners) |

| Back-to-school | $300-800 | $25-67 | Medium (parents) |

| Technology replacement | $200-600 | $17-50 | Low |

You don't need all of these at once. Start with 3-5 categories that are most relevant to your life and add more as your income and savings grow.

4. How to Calculate the Right Amounts

The formula is simple: estimate the annual cost and divide by 12 (or by the number of months until you need it).

Step 1: Review past spending

Look at your bank statements from the past 12 months. How much did you actually spend on car repairs? Holiday gifts? Medical expenses? Real data beats guesses. If you don't have 12 months of data, even 3-6 months gives you a useful baseline.

Step 2: Add a buffer

Add 10-20% to your estimate. Car maintenance might average $1,200/year, but one bad year could be $1,800. A buffer prevents the sinking fund from falling short.

Step 3: Divide by 12

If you expect $1,500 in car costs per year, save $125/month. If holiday gifts cost $800, save $67/month. Simple, predictable, stress-free.

Example: Total sinking fund budget

$510/month sounds like a lot — but you were spending this money anyway, just not on purpose. Sinking funds don't cost more; they prevent the stress and credit card debt that comes from being unprepared.

5. How to Fund Them from Your Current Spending

If $510/month sounds impossible, you probably already have the money — it's just going to other things. Here's how to find it:

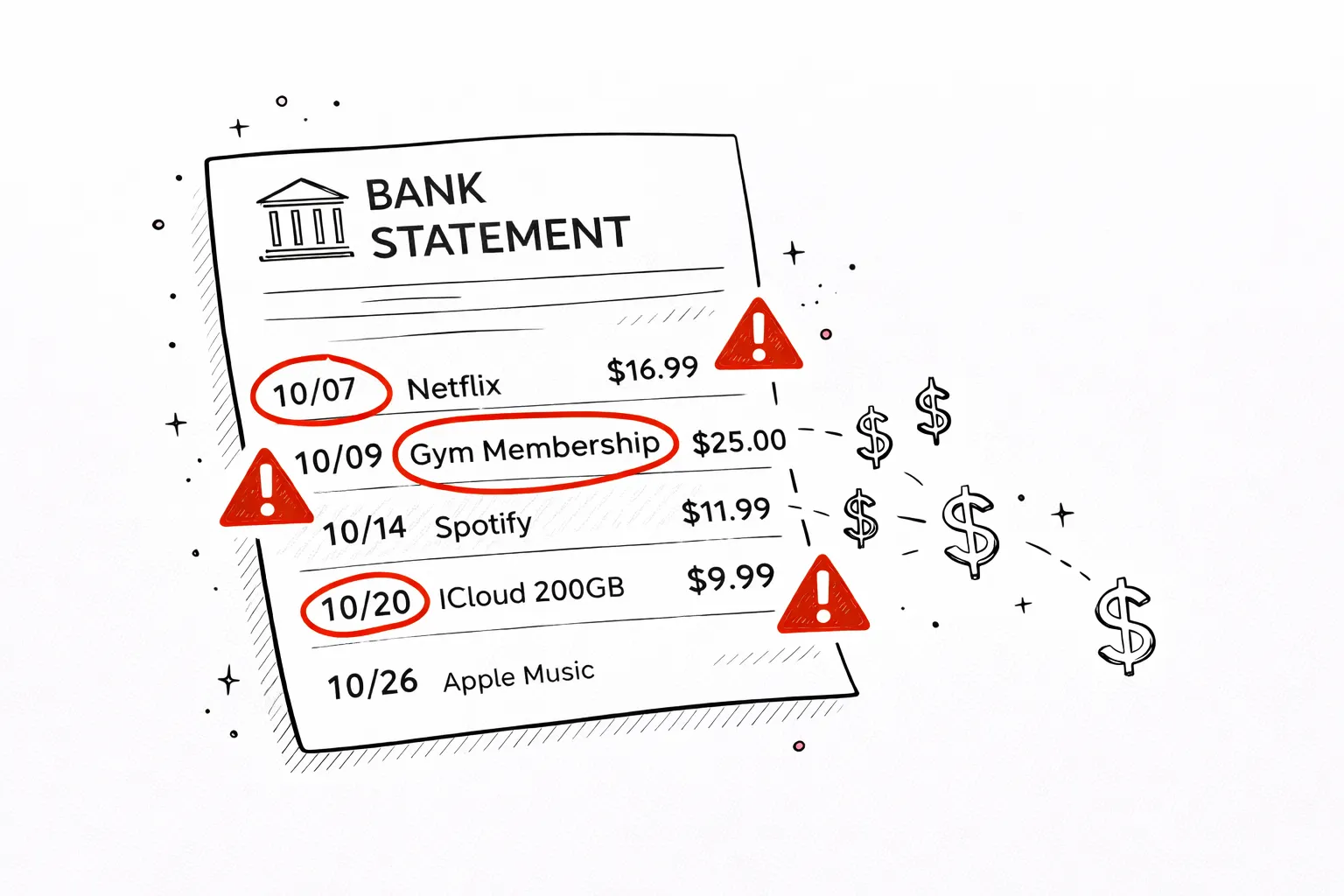

- Upload your bank statement. See exactly where every dollar goes. Most people are surprised by how much they spend on dining out, subscriptions, and impulse purchases.

- Cancel unused subscriptions. The average person has $30-80/month in subscriptions they forgot about. That alone could fund 1-2 sinking fund categories. See our guide on finding hidden subscriptions.

- Reduce dining out by 30%. If you spend $400/month eating out, cutting to $280 frees up $120/month for sinking funds.

- Redirect impulse spending. Every time you resist an impulse buy, transfer that amount to your sinking fund. $15 here, $30 there — it adds up.

- Start small and scale. You don't need to fund all categories immediately. Start with the most urgent 2-3 funds. Add more as you free up cash or as income grows.

6. Where to Keep Your Sinking Funds

Your sinking fund money should be accessible (you'll need it within months, not decades) but separate from your everyday spending money:

The Bottom Line

Sinking funds are one of the simplest, most effective budgeting tools that most people aren't using. They eliminate financial surprises, prevent credit card debt, and make your budget actually work throughout the year — not just in months without big expenses.

Start with your top 3 predictable expenses. Calculate the monthly savings needed. Automate the transfers. Within a few months, those "surprise" expenses will be fully funded — and your financial stress will drop dramatically.

Free tool · 30 seconds · No signup

Find money for sinking funds in your current spending

Upload your bank statement and see exactly where you can redirect spending. Most people find $100-300/month for sinking funds.

Frequently Asked Questions

What is a sinking fund?

A sinking fund is money you set aside each month for a planned future expense. Instead of being surprised by a $1,200 car insurance bill, you save $100/month so the money is ready when the bill arrives. It turns irregular expenses into regular, manageable monthly contributions.

What is the difference between a sinking fund and an emergency fund?

An emergency fund covers unexpected expenses (job loss, medical emergency, car accident). A sinking fund covers expected expenses that are not monthly (car maintenance, holiday gifts, annual insurance, vacation). Emergency funds should not be touched for predictable costs — that is what sinking funds are for.

How many sinking funds should I have?

Start with 3-5 of the most important categories. Common starters are car maintenance, holiday gifts, and medical/dental. You can add more over time, but too many funds at the start spreads your money too thin and makes the system feel overwhelming.

Where should I keep sinking fund money?

A high-yield savings account (HYSA) is ideal — your money earns interest while staying accessible. Some people use separate savings accounts for each fund. Others use one account and track the balances in a spreadsheet. Either approach works.

How do I find money for sinking funds?

Review your bank statement to identify spending you can redirect. Most people find $50-200/month in unused subscriptions, excessive dining out, or impulse purchases that can be redirected to sinking funds instead.