Credit card analysis & CSV export

Credit card statement analyzer

Used by accountants, lenders, and businesses

Encrypted in transitPDF never stored

Works with every card issuer

Why analyze your credit card statement?

Your credit card issuer shows you a list of charges. What they don't show: how much you actually spend on dining vs. groceries vs. subscriptions. A credit card statement analyzer reads your PDF and turns raw charges into categorised, exportable data.

Spot hidden fees

Annual fees, foreign transaction charges, and interest charges buried in your credit card statement — found automatically.

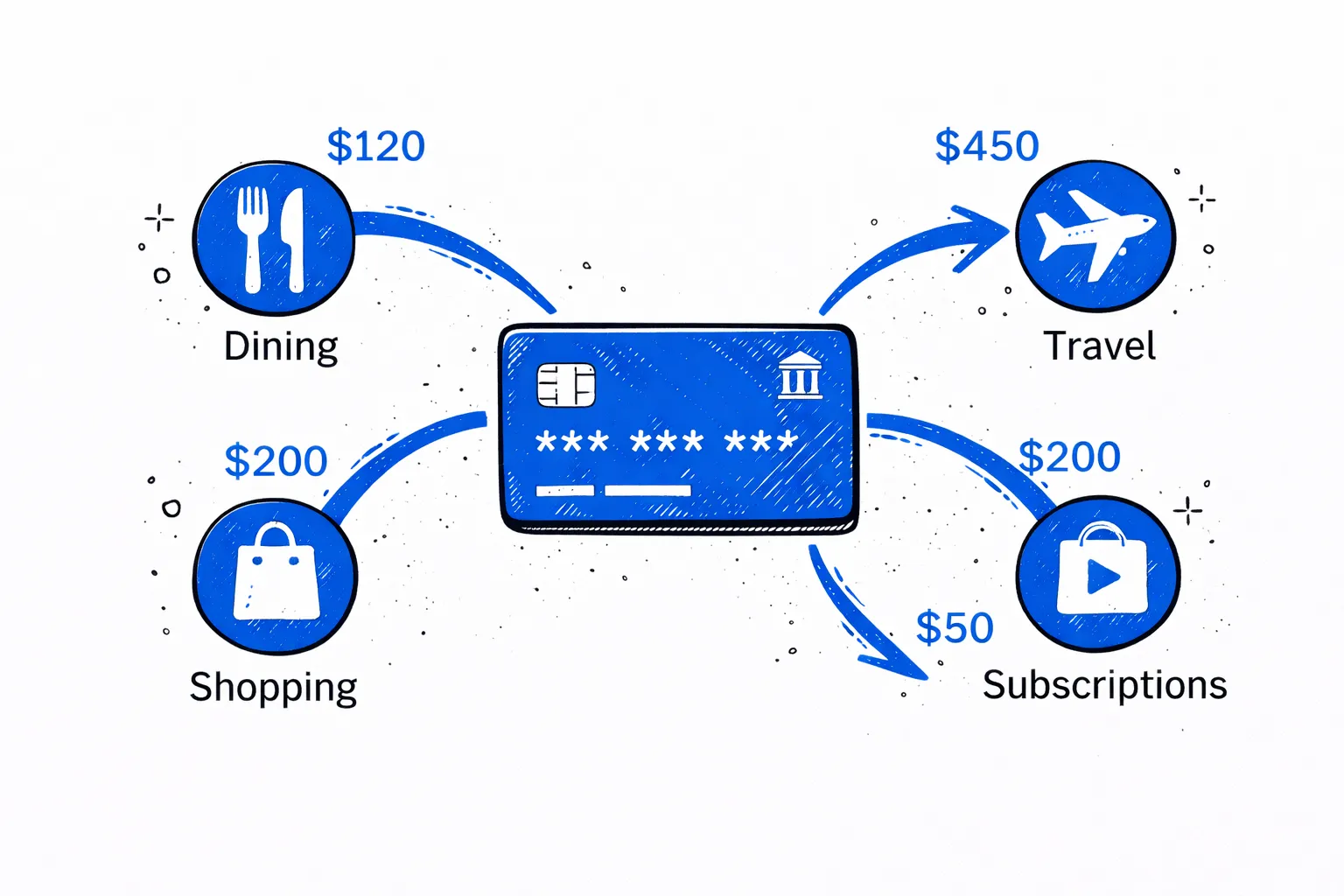

Track spending by category

Dining, travel, shopping, subscriptions — across all your credit card charges.

Export for tax prep

Clean CSV or Excel for your accountant, bookkeeper, or expense report.

Most people use a credit card statement analyzer for one of three reasons: tracking personal spending, preparing business expenses for tax season, or getting a credit card statement to CSV format that accounting software can import.

Your full spending report

Net saved in October 2024

Income

$7,712

Spent

$4,844

Activity

47 tx · ~$103/day

Find money you're leaving on the table

Cancel unused subscriptions

3 services you haven't used in 60+ days

Switch to cheaper phone plan

You're overpaying vs similar usage profiles

Cook 3 more meals per week

You averaged $42/meal eating out — 18 times this month

Ask your statement anything

Dining spending jumped 42% vs last month. You ate out 18 times — that's $42 per meal on average.

See where every dollar went

$4,844 across 7 categories

Your financial health, scored

Spot hidden recurring charges

8 subscriptions found · $349/mo

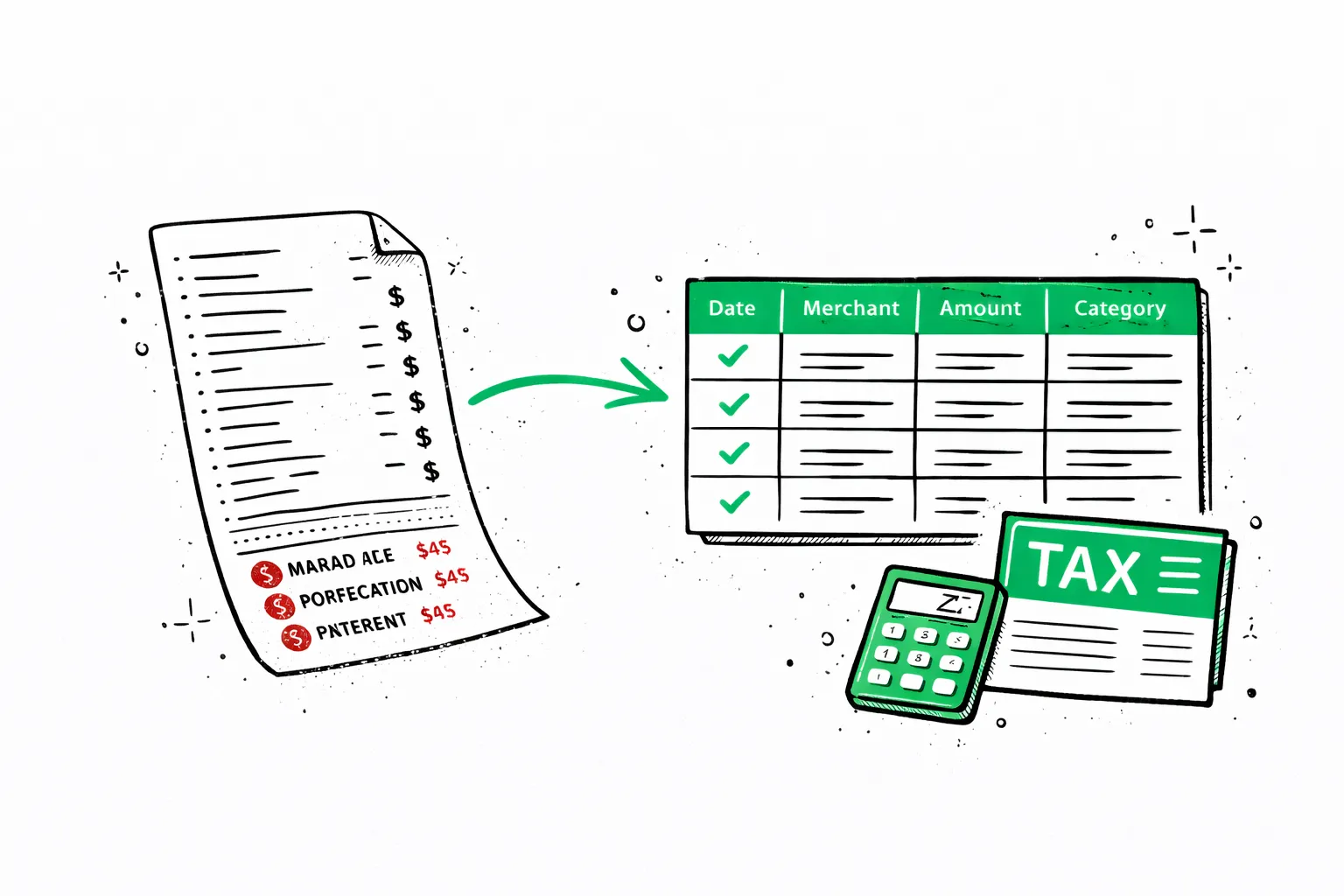

From credit card PDF to Excel in 30 seconds

What your card issuer gives you

What our analyzer gives you

Our credit card spending analyzer reads the PDF, uses AI to categorise every charge — Shopping, Dining, Subscriptions, Travel — and exports a credit card statement to Excel or CSV with one click. Each row includes date, merchant, amount, and category.

Works with Chase, Amex, Capital One, Citi, Discover, and 500+ more card issuers worldwide. Whether it's a personal Visa or a business Amex — upload the PDF, get categorised spending data you can actually use. First page free, no signup.

More than just categories

Real financial clarity from your bank statement.

Subscription tracker

Find the charges you forgot about

AI scans every transaction and flags recurring payments. Most people discover at least one subscription they'd forgotten.

- Detects monthly, annual, and weekly charges

- Shows your true monthly subscription cost

- Spots free trial conversions before they auto-renew

Subscription tracker

Find the charges you forgot about

AI scans every transaction and flags recurring payments. Most people discover at least one subscription they'd forgotten.

- Detects monthly, annual, and weekly charges

- Shows your true monthly subscription cost

- Spots free trial conversions before they auto-renew

AI Insights

Your finances, explained by AI

Get a personalized breakdown of spending habits and anomalies. AI reads every transaction and tells you what actually matters.

- Highlights unusual spending spikes

- Tracks month-over-month trends

- Summarizes financial health in plain English

AI Insights

Your finances, explained by AI

Get a personalized breakdown of spending habits and anomalies. AI reads every transaction and tells you what actually matters.

- Highlights unusual spending spikes

- Tracks month-over-month trends

- Summarizes financial health in plain English

Smart recommendations

Not generic tips — your tips

Every recommendation is based on your actual transactions. Specific dollar amounts, not vague advice.

- Based on your real spending patterns

- Specific dollar amounts you can save

- Actionable in under 5 minutes

Potential monthly savings

$227/mo

Potential monthly savings

$227/mo

Smart recommendations

Not generic tips — your tips

Every recommendation is based on your actual transactions. Specific dollar amounts, not vague advice.

- Based on your real spending patterns

- Specific dollar amounts you can save

- Actionable in under 5 minutes

Analyze your own statement

Upload a PDF, get your full report in 30 seconds.

Statement analyzer pricing

Pro

For heavy files and repeat work

- 200 PDF pages per month

- Unlimited visible transactions per report

- Subscription and recurring charge detection

- Priority support

Business

For lenders, accountants, and teams processing at volume

- 500 PDF pages per month, then $0.08/page

- REST API access with your own keys

- Unlimited visible transactions per report

- Priority support

FAQ