Debt-to-Income Ratio Explained: How to Calculate Your DTI

Your debt-to-income ratio (DTI) is one of the most important numbers in personal finance — and most people have no idea what theirs is. Lenders use it to decide whether you qualify for a mortgage, car loan, or credit card. Here's how to calculate it, what the numbers mean, and how to lower yours if it's too high.

1. What Is Debt-to-Income Ratio?

Your debt-to-income ratio is the percentage of your gross monthly income that goes toward paying debts. It tells lenders — and you — how much of your earnings are already spoken for by existing obligations.

For example, if you earn $6,000 per month before taxes and your total monthly debt payments are $1,800, your DTI is 30%. That means 30 cents of every dollar you earn goes to debt repayment.

DTI matters because it's one of the primary factors lenders use when evaluating loan applications. Unlike your credit score (which measures how reliably you repay), DTI measures how much capacity you have to take on additional debt. A high DTI signals that you're stretched thin — even if you've never missed a payment.

2. The DTI Formula with Examples

The formula is straightforward:

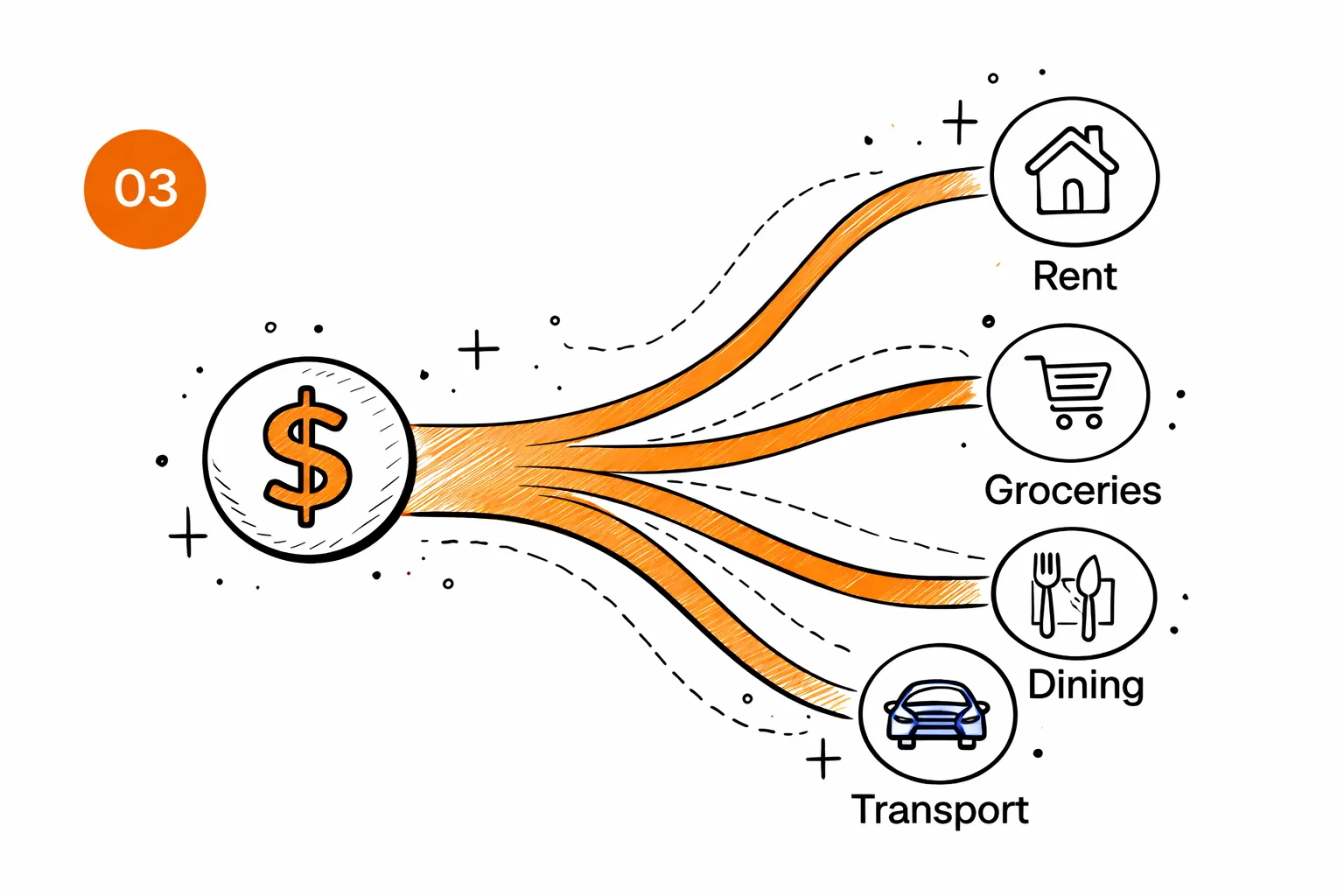

What counts as "debt payments"?

- Mortgage or rent payment

- Car loan payments

- Student loan payments

- Credit card minimum payments

- Personal loan payments

- Child support or alimony

- Any other recurring debt obligation

What does NOT count?

- Utilities (electricity, water, gas, internet)

- Groceries and food

- Insurance premiums (health, life)

- Subscriptions (Netflix, Spotify, gym)

- Transportation costs (gas, transit passes)

Example calculations

| Scenario | Monthly debts | Gross income | DTI |

|---|---|---|---|

| Single, renting | $600 rent + $300 car + $200 student loan = $1,100 | $4,500 | 24% |

| Homeowner | $1,800 mortgage + $400 car + $150 credit card = $2,350 | $7,000 | 34% |

| High debt | $2,200 mortgage + $500 car + $400 student + $300 CC = $3,400 | $6,500 | 52% |

3. What Lenders Consider Good vs Bad DTI

Different lenders have different thresholds, but here's the general consensus:

| DTI Range | Rating | What it means |

|---|---|---|

| Under 20% | Excellent | Very comfortable. You have significant room for new debt. Lenders love this. |

| 20% - 35% | Good | Manageable debt load. You will qualify for most loans with favorable terms. |

| 36% - 43% | Acceptable | Getting tight. You can still qualify for most mortgages, but options narrow. |

| 44% - 49% | High | Risky territory. Conventional mortgages are difficult. Higher interest rates likely. |

| 50%+ | Very High | Half your income goes to debt. Most lenders will decline. Urgent need to reduce debt. |

The magic number for conventional mortgages is 43% — that's the maximum back-end DTI most lenders will accept under the Qualified Mortgage (QM) rule. FHA loans are more flexible, sometimes going up to 50% with strong compensating factors.

4. Front-End vs Back-End DTI

Lenders actually look at two versions of your DTI:

Only includes housing costs: mortgage principal, interest, property taxes, homeowner's insurance, and HOA fees (often called PITI). Most lenders want this under 28%.

Includes housing costs plus all other debt payments: car loans, student loans, credit card minimums, personal loans, child support. Most lenders want this under 36-43%.

Example: Front-end vs back-end

Say you earn $8,000/month gross. Your mortgage (PITI) is $1,600, your car loan is $400, and your student loan is $300.

- Front-end DTI: $1,600 ÷ $8,000 = 20% (excellent)

- Back-end DTI: ($1,600 + $400 + $300) ÷ $8,000 = 28.75% (good)

Both are within healthy ranges. But if you add $500 in credit card minimums, your back-end DTI jumps to 35% — still acceptable but now limiting how much additional mortgage you could qualify for.

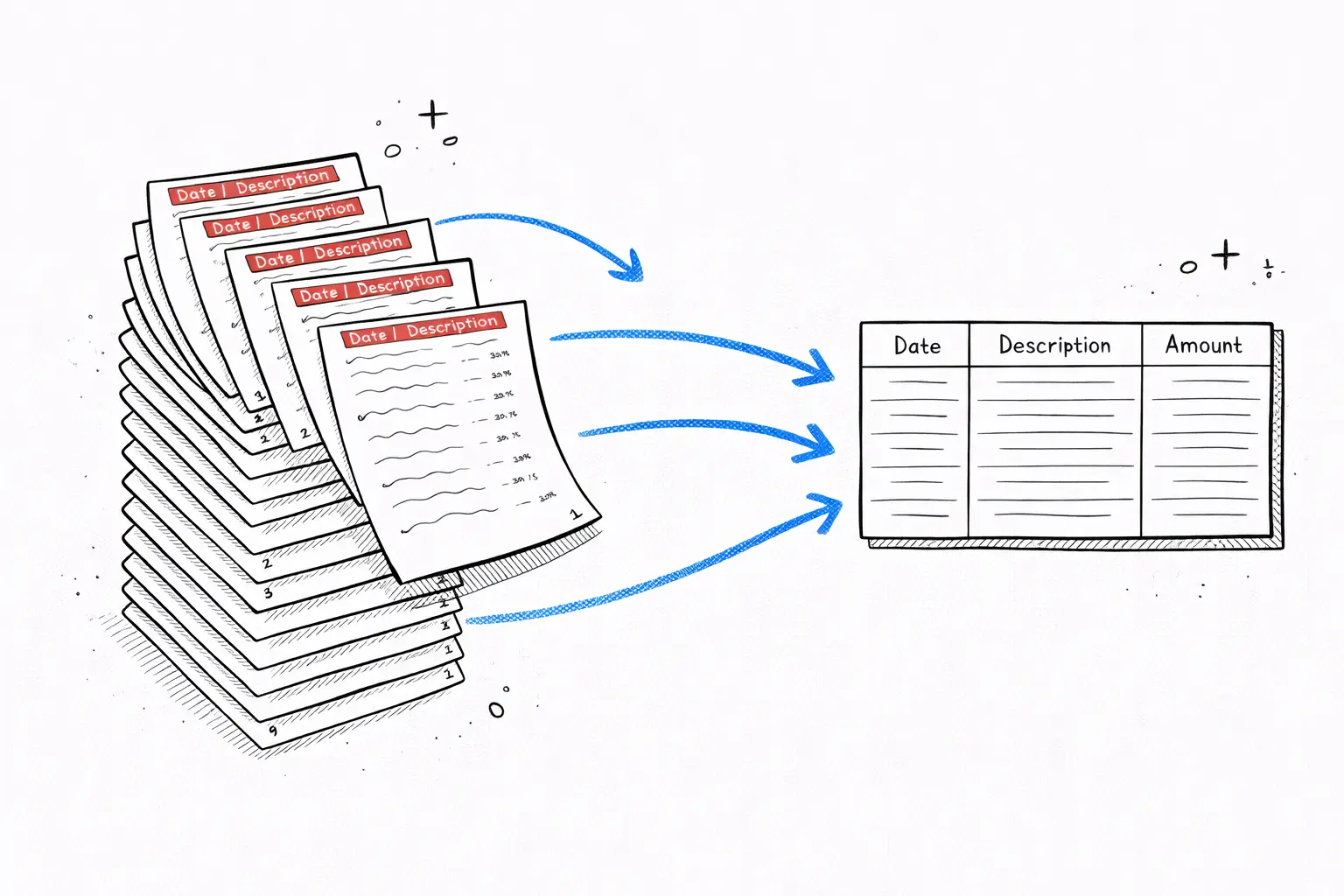

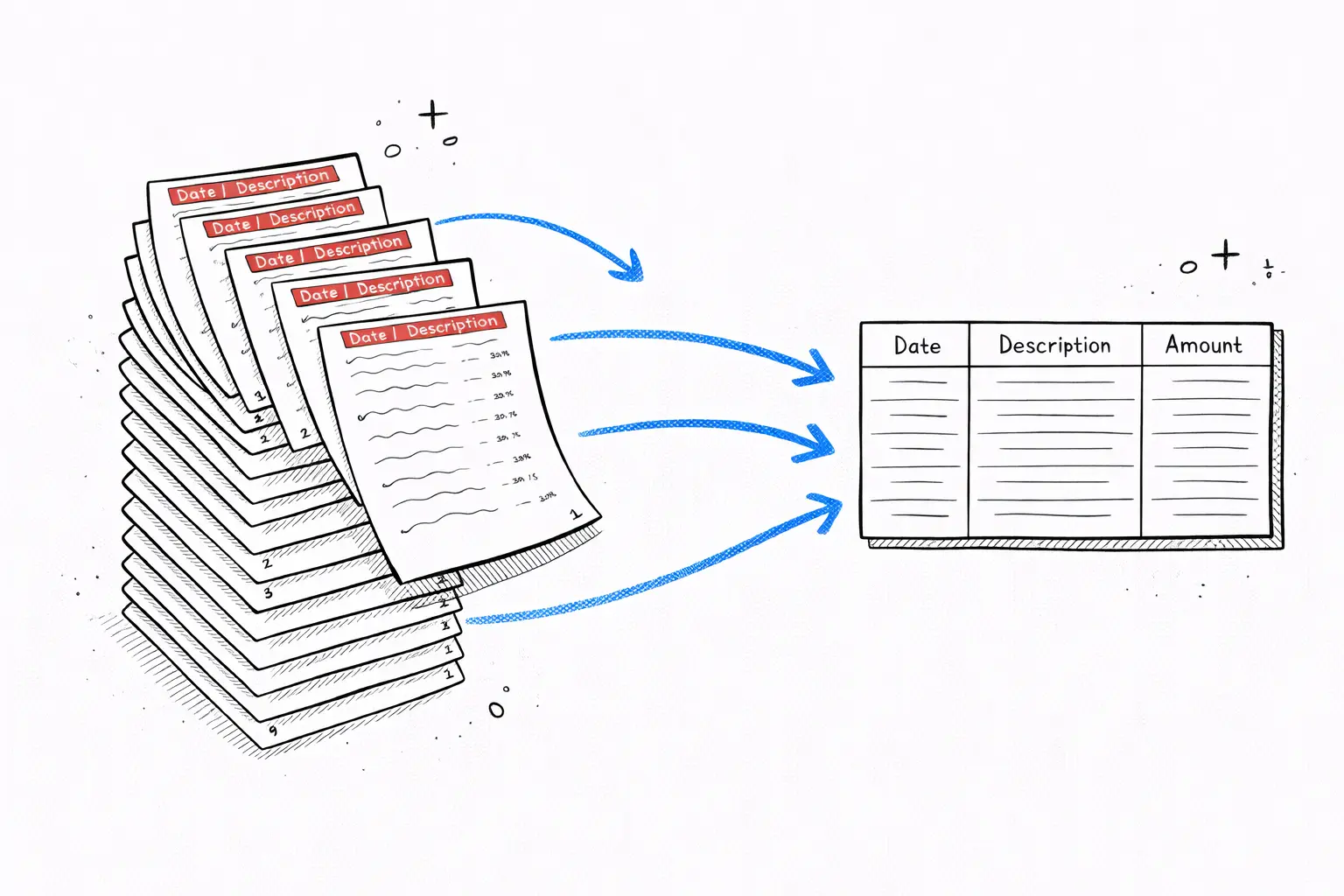

5. How to Calculate DTI from Your Bank Statement

Your bank statement is one of the fastest ways to identify your actual debt payments. Here's how to extract the numbers you need:

- Download your latest statement. Get the full PDF from your bank's website. You want at least one full month.

- Identify recurring debt payments. Look for mortgage/rent, car loan, student loan, personal loan, and credit card payments. These often appear as ACH debits or auto-payments.

- Add up the total. Sum all debt payments for the month. Don't include utilities, groceries, or subscriptions — only actual debt obligations.

- Find your gross income. Look at your direct deposit amounts, then add back taxes and deductions (check your pay stub) to get gross income. Or simply use your annual salary divided by 12.

- Divide and multiply by 100. Total debt payments ÷ gross income × 100 = your DTI percentage.

6. How to Lower Your DTI

If your DTI is too high — especially if you're planning to apply for a mortgage — here are proven strategies to bring it down:

Pay down existing debt

The most direct way to lower DTI. Focus on the debt with the highest interest rate first (avalanche method) or the smallest balance first (snowball method). Every debt you eliminate removes that payment from your DTI calculation entirely.

Increase your income

Since DTI is a ratio, increasing the denominator (income) lowers it. A side hustle, freelance work, overtime, or a raise all help. Even an extra $500/month in documentable income reduces a 40% DTI to about 37%.

Refinance to lower payments

Refinancing a car loan or student loan to a lower rate or longer term reduces your monthly payment — and therefore your DTI. Be careful: extending the term means paying more interest overall, but it can help you qualify for a mortgage now.

Avoid new debt

Every new loan or credit card balance increases your DTI. If you're planning to apply for a mortgage in the next 6-12 months, avoid financing a new car, opening new credit cards, or taking personal loans.

Pay off credit cards completely

Credit card minimum payments count toward DTI. If you can pay off a card in full, that payment disappears from your DTI entirely. Even paying down the balance reduces the minimum payment, which lowers DTI. Use your bank statement analysis to find extra money in your budget for accelerated payoff.

The Bottom Line

Your debt-to-income ratio is a simple calculation with outsized impact. It determines whether you qualify for a home, what interest rate you get, and how much financial flexibility you have. The good news: unlike your credit score, DTI can be improved quickly by paying down debt or increasing income.

Start by calculating yours today. If it's above 36%, make a plan to bring it down. If it's below 28%, you're in great shape — keep it there.

Free tool · 30 seconds · No signup

Calculate your DTI from your bank statement instantly

Upload your statement and see every debt payment categorized automatically. Know your exact DTI in 30 seconds — no spreadsheet required.

Better fit for this topic

Frequently Asked Questions

What is a good debt-to-income ratio?

Most lenders consider a DTI below 36% to be good. Below 28% is excellent. Above 43% makes it very difficult to qualify for a mortgage, though some loan programs allow up to 50% with compensating factors like a high credit score or large down payment.

Does rent count in debt-to-income ratio?

If you rent, your rent payment is not included in your DTI when applying for a mortgage (since the mortgage payment will replace it). However, if you are applying for a different loan while renting, some lenders may consider rent as a recurring obligation.

How do I calculate my DTI from a bank statement?

Add up all monthly debt payments visible on your statement (mortgage/rent, car loan, student loans, credit card minimums, personal loans). Divide that total by your gross monthly income. Multiply by 100 to get your DTI percentage.

What is the difference between front-end and back-end DTI?

Front-end DTI only includes housing costs (mortgage, property tax, insurance, HOA). Back-end DTI includes all monthly debt obligations. Lenders look at both, but back-end DTI is the more important number for loan qualification.

Can I get a mortgage with a 50% DTI?

It is very difficult but not impossible. FHA loans allow DTI up to 50% with compensating factors. Conventional loans typically cap at 43-45%. A high DTI means you will likely get a higher interest rate and smaller loan amount.