How to Find Income from Bank Statements

A practical method for turning bank statement deposits into a reliable income estimate. Learn how to separate payroll, benefits, self-employed income, transfers, refunds, and one-off deposits.

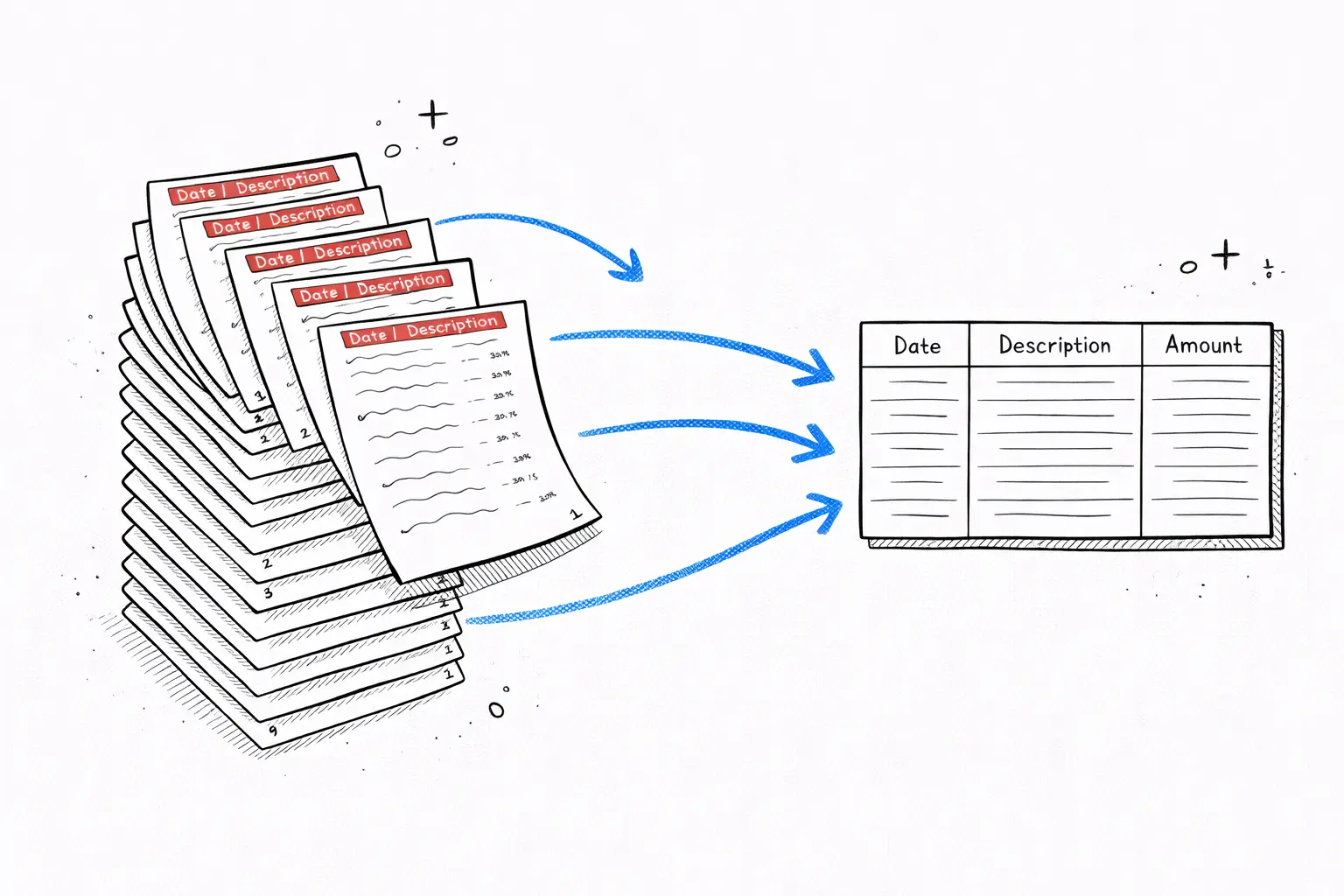

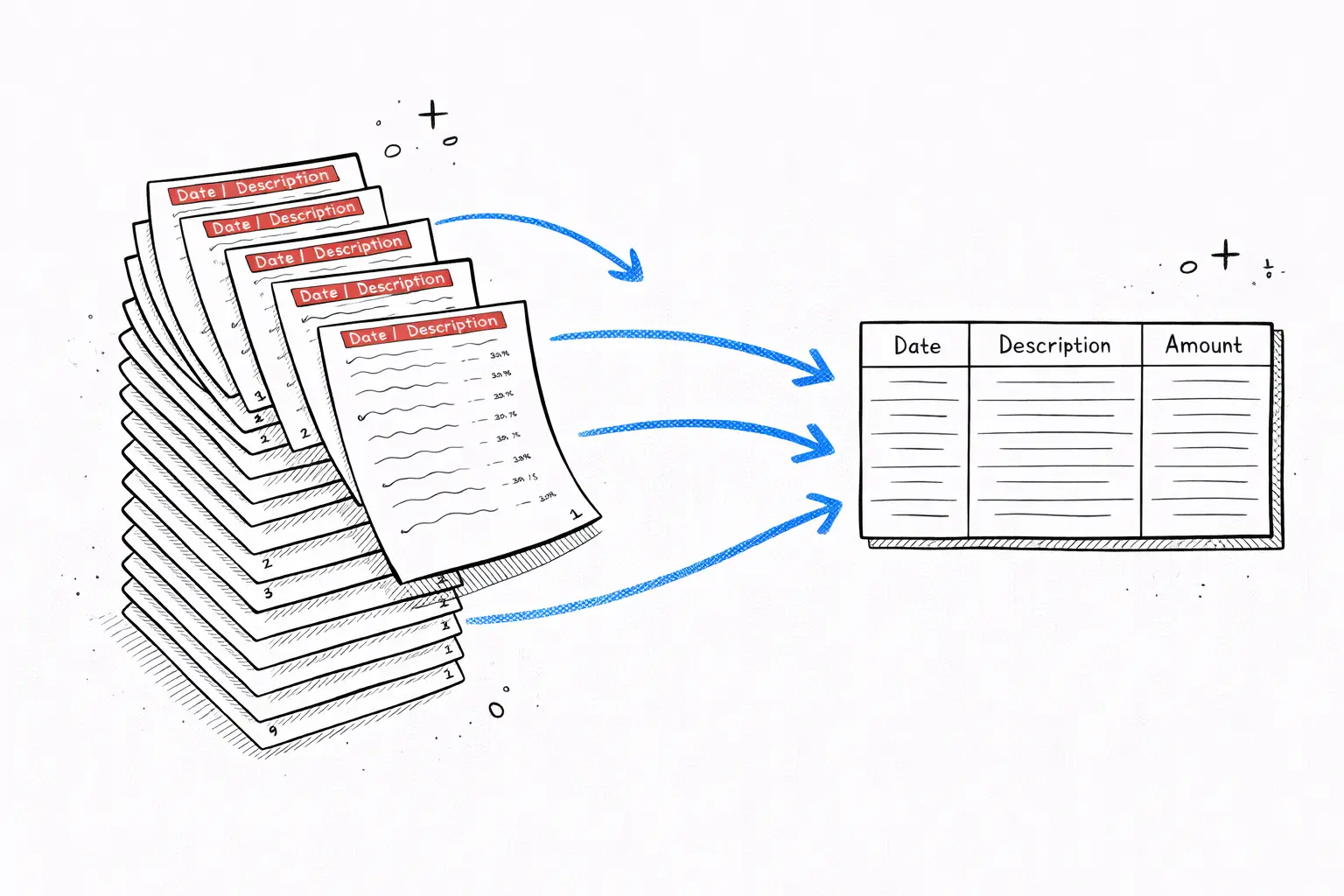

To find income from bank statements, count recurring deposits from real payers and exclude transfers, refunds, reversals, loan proceeds, and one-off credits. Group deposits by source, total the qualifying income, then divide by the number of months reviewed.

Reviewed against current mortgage asset-verification guidance, consumer-banking guidance, and official immigration-financial-evidence materials where relevant. Requirements still vary by lender, bank, country, and reviewer, so use this as preparation guidance rather than legal or underwriting advice.

What counts as income on a bank statement

Income is money earned or received from a genuine external source. On a bank statement, it usually appears as payroll, pension, benefits, client payments, rental income, platform payouts, or recurring business revenue.

The hard part is not finding credits. The hard part is deciding which credits are income. A statement may show transfers, refunds, loan advances, cashback, reversals, and temporary deposits that increase the balance but should not be treated as earnings.

Step-by-step income calculation

- Collect the full review period. Use complete monthly statements, not screenshots or partial exports.

- List every credit. Pull deposit date, description, payer, and amount into a spreadsheet or analyzer.

- Remove obvious non-income. Exclude transfers, refunds, chargebacks, reversals, loan proceeds, and internal movement between accounts.

- Group deposits by payer. Payroll should cluster around the same employer. Self-employed income may cluster by client, platform, processor, or business account.

- Separate regular and irregular income. Payroll and monthly benefits are easier to annualize than bonuses, seasonal work, or one-off client payments.

- Calculate the average. Add qualifying income and divide by the number of months reviewed.

How to classify common deposits

| Deposit type | Usually count? | Notes |

|---|---|---|

| Employer payroll | Yes | Strong income evidence when name, amount, and frequency are consistent. |

| Government benefits or pension | Yes | Match to award letter, benefit letter, or pension statement if needed. |

| Self-employed client payments | Usually | Count recurring business revenue, but separate gross receipts from net income when a lender requires it. |

| Marketplace or platform payouts | Usually | Group by platform and review enough months to smooth seasonality. |

| Transfers from your own account | No | Only traceable movement of money you already had. |

| Tax refund | No | Useful cash, but not recurring monthly income. |

| Loan proceeds | No | Borrowed money is not income and may create a liability. |

| Cash deposits | Maybe | Needs invoices, receipts, or a credible written trail. |

Example monthly income worksheet

Suppose you review three months of statements. You find payroll deposits of $4,200, $4,200, and $4,200, a tax refund of $1,100, and a transfer from savings of $2,000.

The income estimate is $12,600 divided by 3 months, or $4,200 per month. The tax refund and transfer are useful cash-flow context, but they should not inflate recurring income.

Mistakes that overstate income

- Counting transfers from savings as new income.

- Counting refunds, reversals, or chargebacks as earnings.

- Using gross business deposits as personal income without accounting for expenses.

- Annualizing a one-time bonus as if it happens every month.

- Ignoring missing months or partial statements.

Free tool · 30 seconds · No signup

Upload a statement.

See where every dollar goes.

AI reads your bank PDF, categorizes every transaction, finds subscriptions you forgot about, and exports everything to CSV.

Frequently asked questions

Yes, a bank statement can support income when deposits clearly show regular payroll, benefits, business revenue, rent, pension, or other recurring sources. It is stronger when paired with pay stubs, invoices, tax records, contracts, or benefit letters.

Usually no. Transfers between your own accounts do not create new income. Count them only if you can prove the sending account received income first and the transfer is part of the same traceable flow.

Use at least three months for a quick estimate. Use six to twelve months when income is seasonal, self-employed, commission-based, or irregular.

Usually no. A refund is money returned from a previous purchase, tax overpayment, or adjustment. It can increase cash available, but it should not be treated as recurring income.

Add only qualifying income deposits for the review period, exclude transfers and one-off non-income credits, then divide by the number of months reviewed. Keep a separate note for bonuses or seasonal income.